Crypto-related equities are sliding hard, with some of the sector’s biggest names giving up a large part of their previous bull‑market gains as selling pressure intensifies across digital assets.

Shares of IREN, a Bitcoin mining firm that has been pivoting into AI data-center infrastructure, fell another 6.5%, briefly touching around $42. From its peak, the stock is now down more than 47%, with traders bracing for the company’s upcoming earnings report. Other mining groups have not escaped the rout: MARA and Bitfarms have also sold off sharply, mirroring the weakness in the underlying crypto market.

The pain is even more visible in bellwether crypto proxy stocks. Michael Saylor’s MicroStrategy (MSTR), widely seen as a leveraged bet on Bitcoin because of its massive BTC treasury, has tumbled to roughly $110. That’s a dramatic decline from its all-time high near $550 and has slashed the company’s market capitalization to about $38 billion, down from more than $130 billion at the peak.

Crypto exchanges, which typically boom when trading volumes are high and enthusiasm is elevated, are under similar pressure. Coinbase has dropped to around $150 after previously hitting a record near $443. Newer publicly listed rivals such as Bullish and Gemini have also slid to fresh lows, underlining how broad-based the sector’s downturn has become.

The common driver behind these moves is the ongoing sell-off in Bitcoin and major altcoins. As prices have fallen, leveraged traders have been forced out of positions, triggering a wave of liquidations. Total liquidations recently surged by about 74% to approximately $1.4 billion, amplifying volatility and accelerating the downward move in both tokens and related equities.

The linkage is straightforward: crypto operating companies are effectively high-beta plays on the digital asset market. When Bitcoin and alternative coins trend higher, miners such as IREN and MARA see revenue rise because the coins they produce and hold become more valuable. Their margins expand, balance sheets look stronger, and investors are willing to pay higher multiples for future growth.

In a bear phase, the dynamic flips. The same miners still face relatively fixed costs for energy, hardware, and infrastructure, but the market value of the Bitcoin they generate declines. If prices fall far enough, some mining operations approach breakeven or negative profitability, causing investors to reassess the sustainability of their business models and sharply discount their shares.

For exchanges like Coinbase, Gemini, and Bullish, the primary risk is not just price direction but trading activity itself. The bulk of Coinbase’s income is still derived from transaction fees, with a smaller slice coming from subscription products and various services. Gemini and Bullish are even more transaction‑dependent, generating more than 90% of their revenue from trading fees. In risk‑off environments, retail and institutional traders pull back, trading volumes shrink, and fee revenues contract, which investors quickly price in.

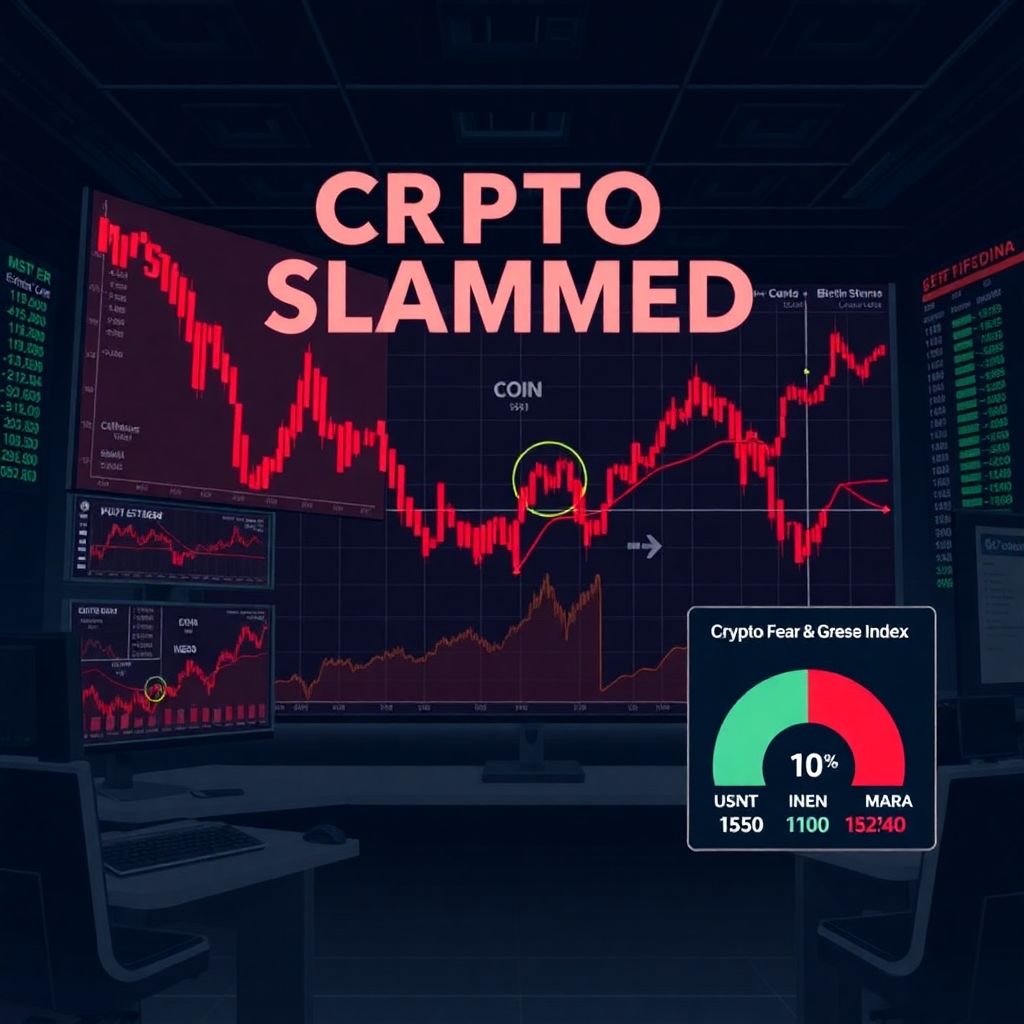

Sentiment indicators confirm how deeply negative the mood has become. The widely watched Crypto Fear and Greed Index has plunged into the “extreme fear” zone, hitting levels near 10. Historically, readings this low have often coincided with, or slightly preceded, major market turning points, as capitulation selling exhausts itself and value buyers begin to step in.

From a technical perspective, many large‑cap coins, including Bitcoin and Ethereum, now appear heavily oversold on daily and weekly charts. Momentum oscillators and relative-strength gauges have dropped into zones that, in past cycles, have been followed by sizeable relief rallies. While technical oversold conditions do not guarantee an immediate bottom, they suggest the downside may be increasingly limited relative to potential upside once sentiment stabilizes.

Geopolitics is adding another layer of uncertainty. Markets are nervously watching the possibility of a US strike on Iran under a Trump administration, an event some investors see as a near‑term risk for risk assets. Concerns over such an escalation have contributed to the current bout of risk aversion, undermining crypto prices and, by extension, crypto‑linked stocks.

Ironically, scenarios like this can produce a “sell the rumor, buy the news” pattern. If a strike were to occur, digital assets and related equities could see another sharp leg down on the initial headline shock, followed by a rebound once the scale of the event is clearer and worst‑case fears are either confirmed or dismissed. A similar pattern played out during the 12‑day conflict in June last year, when crypto assets initially slumped and then staged a recovery.

Why crypto stocks move more violently than Bitcoin

One reason names like MSTR, COIN, IREN, and MARA appear to “overshoot” Bitcoin’s moves is leverage—both explicit and implicit. MicroStrategy’s balance sheet is heavily exposed to BTC, which turns its equity into a geared instrument: a 10% move in Bitcoin can translate into a far larger percentage move in the stock. Miners face something similar: their future production is effectively a leveraged claim on future Bitcoin prices, so equity investors price in not only current spot prices but expectations for profitability over the coming years.

For exchanges, the leverage is operational. Their profits tend to rise faster than volumes in bull markets because of operating leverage, and they fall faster when volumes decline in bear markets. That operating leverage makes their share prices highly sensitive to changes in sentiment and trading activity, often producing bigger swings than the underlying crypto indices.

The role of liquidations and derivatives

The spike in liquidations shows how derivatives markets can magnify both rallies and crashes. When traders pile into leveraged long positions and prices move against them, exchanges automatically close those positions once collateral is insufficient, effectively forcing them to sell into a falling market. This cascades into more selling and more liquidations, depressing prices further and exacerbating stress in publicly traded crypto firms whose valuations depend on spot prices and sentiment.

On the flip side, once the bulk of leveraged longs have been flushed out, the market structure often becomes healthier. With fewer weak hands left, even modest positive catalysts—such as better‑than‑feared economic data, a dovish shift in central bank rhetoric, or improving on‑chain metrics—can trigger outsized rebounds as shorts cover and sidelined buyers re‑enter.

What this means for investors in crypto stocks

For investors holding or considering positions in MSTR, COIN, IREN, MARA, and similar names, the current environment underscores the need for a clear risk framework. These equities tend to be more volatile than Bitcoin itself, so position sizing, diversification, and the use of stop‑losses or options hedges become crucial. Long‑term investors who believe in the structural growth of the crypto ecosystem may view deep drawdowns as an opportunity to accumulate, but they must be prepared for extended periods of turbulence.

Fundamentals also matter more in tougher markets. For miners, balance sheet strength, energy costs, geographic diversification, and efficiency of hardware fleets can determine who survives a prolonged downturn. For exchanges, the breadth of revenue sources—such as custody, institutional services, staking, or subscription offerings—can help cushion the blow from reduced trading volumes.

Is the crypto crash close to an end?

Calling a precise bottom is impossible, but several ingredients that have historically appeared near major turning points are present: extreme fear readings, oversold technicals, elevated liquidations, and broad capitulation in high‑beta crypto equities. At the same time, macro uncertainty and geopolitical risks remain unresolved, and further negative headlines could still push prices lower before a durable base is formed.

Investors often look for confirmation signals: stabilization in Bitcoin’s price around key long‑term moving averages, a slowdown in liquidations, improvement in funding rates, and evidence that selling pressure in crypto stocks is easing. When these signs begin to align, it can indicate that the worst of the crash is behind the market, even if the path back to previous highs is long and uneven.

The longer‑term context: crypto cycles and equity proxies

The current slump fits into the broader pattern of crypto market cycles, where euphoric upswings are typically followed by sharp corrections. Over multiple cycles, each peak and trough has drawn in more institutional capital, more regulatory scrutiny, and more sophisticated infrastructure. Crypto‑linked stocks have gradually become a preferred way for some traditional investors to gain exposure to the asset class without directly holding tokens.

As the industry matures, the correlation between these stocks and Bitcoin may evolve. Companies that successfully diversify into adjacent areas—such as AI data centers in the case of IREN, or broader financial services platforms in the case of exchanges—could, over time, become less purely dependent on Bitcoin’s price and more on their own execution and innovation.

For now, however, the message from the market is clear: during deep crypto drawdowns, even the sector’s most prominent equities can suffer extreme volatility. Whether this phase marks the final leg of the current crash or just another step down, the fate of MSTR, COIN, IREN, MARA, and their peers remains tightly bound to the next major move in Bitcoin and the broader digital asset universe.