Strategy’s evolution from an enterprise software vendor into the world’s most aggressive corporate Bitcoin accumulator has reshaped how publicly traded companies think about their treasuries. Over a little more than five years, the firm led by Michael Saylor has turned a bold hedge against inflation into a full‑blown Bitcoin operating strategy, amassing one of the largest single stashes of BTC on the planet.

Instead of keeping excess cash in dollars or short‑term bonds, the company gradually reoriented its balance sheet around Bitcoin. The stated goal was simple but radical for a listed firm: use Bitcoin to “maximize long‑term value for shareholders.” In practice, that meant opportunistically buying BTC during bull markets, bear markets, and everything in between—often with borrowed money or equity raises—whenever management believed the risk‑reward profile was favorable.

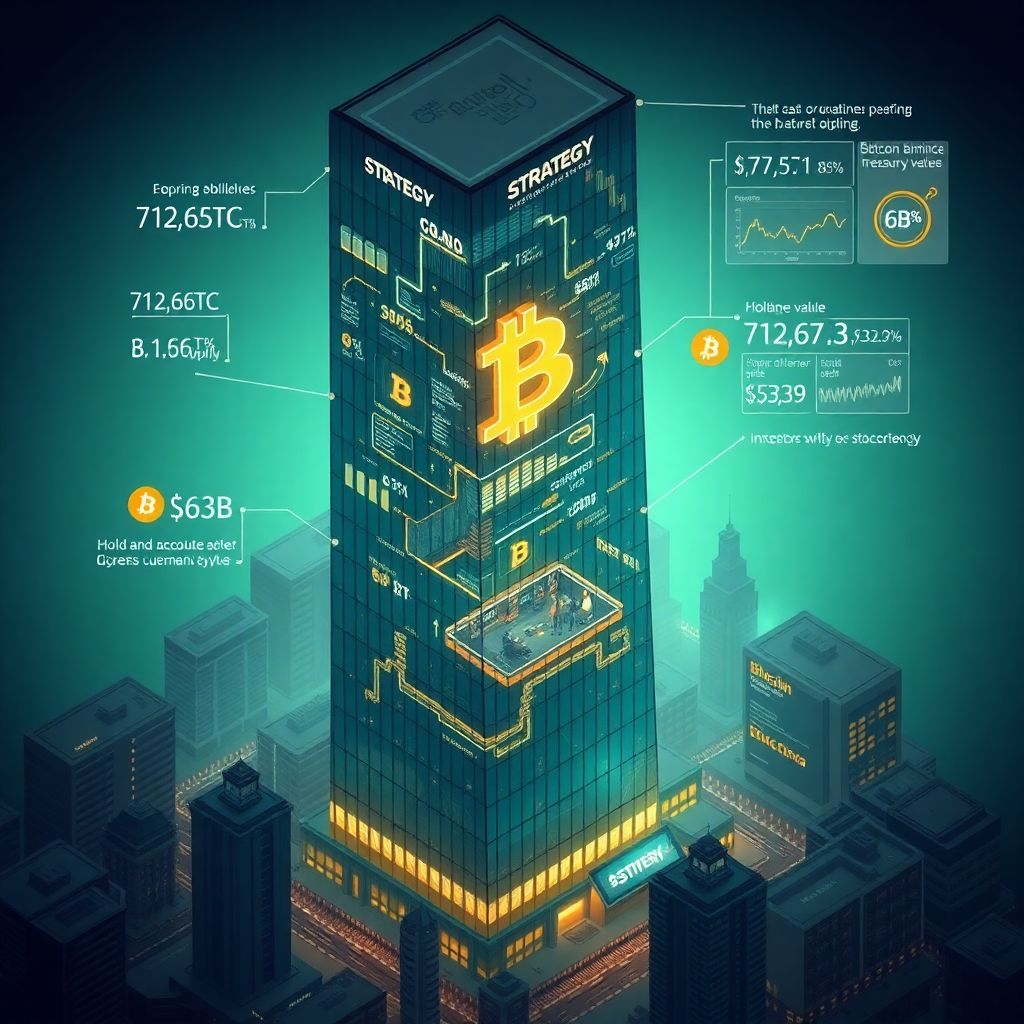

As a result, Strategy now controls 712,647 BTC, representing close to 3.4% of Bitcoin’s hard‑capped 21 million supply. At current market levels, that hoard is valued at roughly $63 billion, turning the company’s stock into a de facto Bitcoin proxy for many traditional investors who prefer not to deal with self‑custody or direct exposure to crypto exchanges.

The journey to that number is marked by a series of blockbuster purchases that reveal how aggressively the firm scaled its conviction over time. Its single largest acquisition to date came on November 25, 2024, when the company added a remarkable 55,500 BTC in one move. That buy alone would put Strategy among the largest corporate holders in the world even if none of its other purchases existed.

Just a week earlier, on November 18, 2024, the firm executed what is now its second‑largest haul: 51,780 BTC. Two such massive purchases in the span of days underscored how committed management had become to using every available financing channel—debt, equity issuance, and retained earnings—to expand its Bitcoin position whenever market conditions aligned with its thesis.

The company’s third‑largest buy dates back to the previous cycle. On December 21, 2020, Strategy acquired 29,646 BTC, capitalizing on a period when institutional interest in Bitcoin was just beginning to accelerate. That acquisition signaled early that this wasn’t a one‑off balance sheet experiment but the foundation of a sustained Bitcoin accumulation strategy.

The fourth biggest purchase came again during the late‑2024 buying spree. On November 11, 2024, Strategy picked up 27,200 BTC, continuing a rapid expansion phase that turned the final quarter of 2024 into one of the most aggressive accumulation windows in the company’s history.

The remaining top buys show that the program did not slow as the market matured and prices climbed. On January 20, 2026, the company added another 22,305 BTC, its fifth‑largest single acquisition. Less than a year earlier, on March 31, 2025, it secured 22,048 BTC, underscoring a pattern: Strategy consistently treated Bitcoin not as a trade but as a strategic reserve asset to be accumulated irrespective of short‑term volatility. Another large move came on December 9, 2024, when the firm purchased 21,550 BTC—its seventh‑largest haul and part of the same multi‑month wave that dramatically expanded its holdings.

Each of these outsized buys was typically financed through a mix of corporate tools more commonly associated with traditional capital management than crypto speculation. Strategy issued convertible notes, raised equity, and tapped existing cash flows, effectively turning its balance sheet into a leveraged bet on Bitcoin’s long‑term appreciation. The wager is that Bitcoin will outperform both inflation and conventional store‑of‑value assets over a multi‑year horizon.

From a market structure perspective, one company locking up nearly 3.4% of the total eventual Bitcoin supply is significant. Bitcoin’s fixed 21 million cap means that large, long‑term holders can meaningfully influence available float and liquidity. Strategy’s policy of treating BTC as a permanent treasury asset—not inventory to be traded in and out of—removes a substantial amount of coins from regular circulation, potentially amplifying scarcity effects during bullish periods.

Strategy’s transformation has also altered how investors value the business itself. For many, its stock serves as a leveraged play on Bitcoin price movements: when BTC rallies, the notional value of the company’s holdings can surge by billions, often outpacing the underlying software revenue in terms of impact on market capitalization. Conversely, sharp drawdowns in Bitcoin can exert significant pressure on the company’s share price and balance sheet metrics, especially given mark‑to‑market accounting rules and interest obligations on issued debt.

This aggressive posture has turned the firm into a high‑beta vehicle on Bitcoin rather than a conventional software play. That dual identity attracts a unique shareholder base: some investors are primarily interested in exposure to BTC via a regulated equity; others see upside in the core business enhanced by the optionality of a massive Bitcoin treasury during future bull cycles.

For other corporate treasurers, Strategy’s experience serves as both inspiration and cautionary tale. On the one hand, the firm has demonstrated that a convicted, long‑term Bitcoin strategy can yield enormous nominal gains when the asset appreciates. On the other, it has had to weather periods of severe drawdowns where the market value of its holdings fell far below acquisition cost—tests of both shareholder patience and boardroom resolve.

Regulatory and accounting environments also play a crucial role. Navigating disclosures, impairment rules, and evolving guidance on digital assets has required a high tolerance for legal and financial complexity. Companies considering a similar route must be prepared for increased scrutiny from auditors, regulators, and investors who may be unfamiliar or uncomfortable with significant crypto exposure on a public company balance sheet.

Another critical factor is risk management. Strategy’s approach has been unusually aggressive by traditional standards, including the use of leverage to buy Bitcoin. While this amplified returns during uptrends, it also elevated downside risk. More conservative firms exploring BTC for their treasuries might limit exposure to a small percentage of total assets, avoid leverage, and treat Bitcoin as a diversified hedge rather than the core of their capital structure.

At a macro level, the Strategy playbook has contributed to a broader shift in how Bitcoin is perceived. What began as an experiment in digital money is increasingly framed as a corporate reserve asset akin to digital gold. The entrance of listed companies—alongside institutional funds and exchange‑traded products—has tightened the link between traditional financial markets and crypto, creating feedback loops between equity valuations, credit markets, and Bitcoin’s price.

Looking ahead, the sustainability of Strategy’s approach will depend on a few key variables: Bitcoin’s long‑term price trajectory, the cost and availability of capital, regulatory clarity, and the performance of its underlying software operations. If Bitcoin continues to grow as a macro asset class, the company’s early and aggressive positioning could remain a powerful tailwind. If not, the same strategy could be seen as an overextended concentration risk.

For now, the numbers speak to the scale of the bet: 712,647 BTC, acquired through years of steady and often spectacular buying, worth around $63 billion at current prices and accounting for a meaningful slice of the asset’s fixed supply. The seven largest purchases—ranging from 21,550 BTC to 55,500 BTC—trace the arc of a corporate strategy that has placed Bitcoin at the very heart of its identity, balance sheet, and future.