Why Liquidity Pools Pay You — And Where the Catch Is

If you’ve ever looked at DeFi yields and thought “this is too good to be true,” impermanent loss is a big part of the catch. When you drop tokens into a liquidity pool on Uniswap, Curve or another AMM, you’re not just “parking” assets — you’re agreeing to let a formula rebalance your coins as prices move. That rebalancing is what quietly eats into your profit. The goal of this article is not to scare you away from pools, but to show how this hidden mechanism works in practice so you can use it on your own terms, not the other way around.

In plain language, impermanent loss is the difference between what you’d have if you simply held your tokens versus what you actually have inside the pool after prices move. It’s “impermanent” only as long as you don’t withdraw; the moment you pull the liquidity out, the difference becomes very real and very permanent.

Key Terms Without the Jargon Fog

Liquidity Pool

A liquidity pool is just a shared pot of tokens locked in a smart contract. Traders swap against this pot instead of using an order book with buyers and sellers. In a typical 50/50 pool like ETH/USDC, the pool starts with equal value of both tokens. The smart contract uses a formula to decide the price and how much of each token sits in the pot. In return for contributing, you get LP tokens, which are like a receipt proving your share of the pool and your right to a slice of the trading fees.

Think of it like a vending machine that refills and reprices itself automatically. You and other LPs stock the machine with snacks (tokens). Traders take snacks and put in money (other tokens). The machine always keeps a certain balance between snack A and snack B, and changes the “exchange rate” every time someone buys or sells.

Automated Market Maker (AMM)

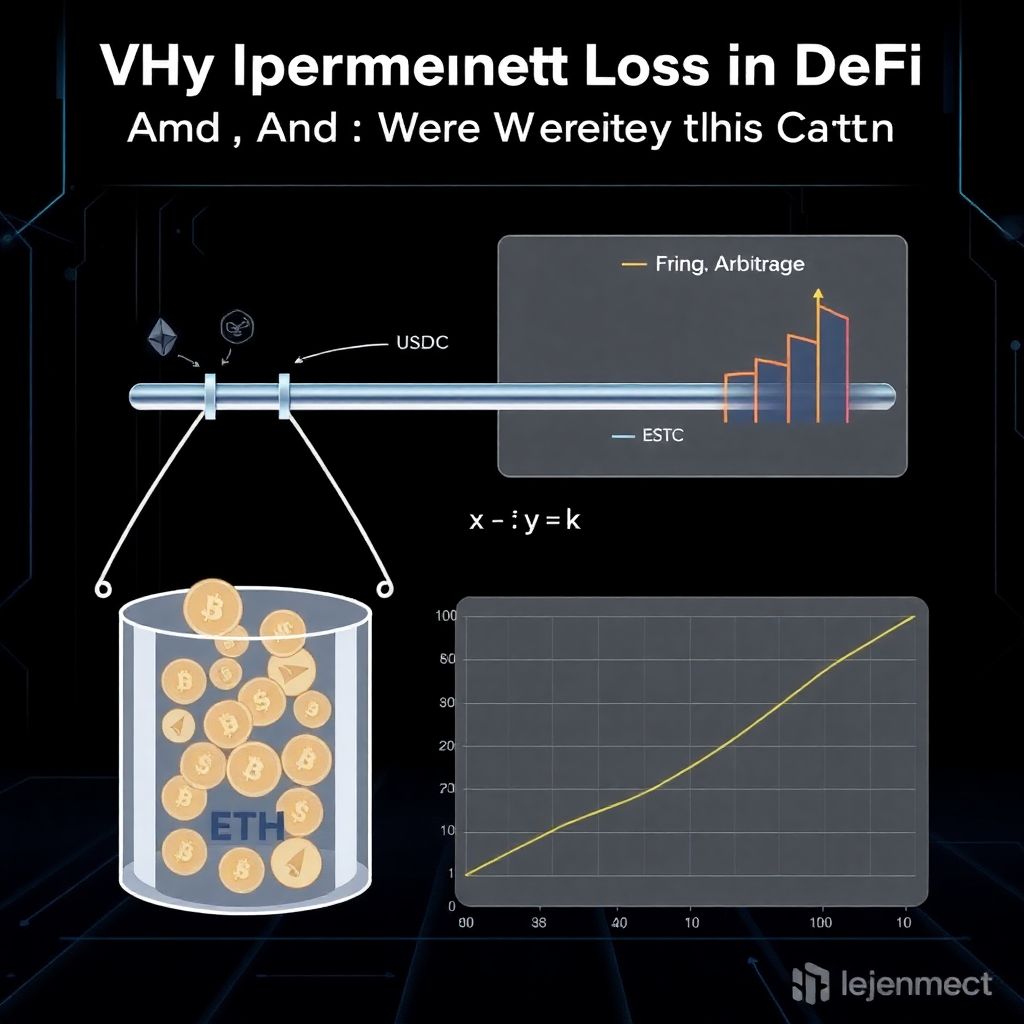

Most DeFi liquidity pools today are run by something called an Automated Market Maker. The most famous is the constant product formula: x * y = k. Here x is the amount of token A in the pool, y is the amount of token B, and k is a constant. When a trade happens, x and y change, but their product stays the same. The math forces the price to move as trades happen — no centralized market maker needed.

You can picture it as a seesaw where the product of the distances to the pivot must stay the same. If someone pushes one side up (buys a lot of token A), the other side must go down in a way that keeps the total “torque” constant. Impermanent loss appears because the seesaw keeps moving your holdings to balance itself, even if you would rather just sit still and hold.

Impermanent Loss

Impermanent loss is the loss you experience because the pool automatically rebalances your tokens when the price moves, compared to just holding the tokens in your wallet. If the relative price between the two assets changes, the pool will end up with more of the cheaper token and less of the more expensive one. As a liquidity provider, you own a slice of that new mix — usually not the mix you would have chosen.

It’s called “loss” not because you necessarily end up with less money overall, but because you end up with less than the simple HODL strategy would have given you. Trading fees and incentives can still push you into profit, but impermanent loss drags you in the opposite direction.

Visualizing Impermanent Loss: Diagrams in Words

Diagram 1: The Two Lines That Matter

Imagine a simple graph. The horizontal axis is “price change of token A vs token B.” At the center, price ratio is 1 (no change). Move to the right: token A becomes more expensive than token B. Move left: token A gets cheaper. Now, draw two curves. The first is a straight diagonal line starting at the origin: that’s your value if you just hold both tokens — your wealth goes up or down linearly with price. The second curve is a bowed line under that diagonal: that’s your wealth as a liquidity provider. The gap between the straight line and the bowed line is your impermanent loss.

On this mental chart, the more the price moves away from the starting point, the wider the gap between the lines. Small price moves mean the two lines almost overlap, so impermanent loss is tiny. Big rallies or crashes bend the AMM curve away from the diagonal, showing you’re lagging behind the simple holder who just watched the show from the sidelines.

Diagram 2: Token Buckets

Picture two transparent buckets connected by a rigid bar, one labeled ETH, the other USDC. Inside each bucket is a pile of tokens. At the start, both piles are the same value. The bar between the buckets enforces the rule “ETH_amount × USDC_amount = constant.” When traders buy ETH, they scoop ETH out of the ETH bucket and pour USDC into the USDC bucket. The bar then magically pushes the buckets into a new position to restore the constant product.

If the price of ETH goes up on the broader market, arbitrage traders will keep scooping ETH from the pool and adding USDC until the pool’s price matches the market. You, as LP, end up with a smaller ETH pile and a bigger USDC pile. From the outside, your combined value might have grown thanks to higher ETH price and fees, but it’s still less than if you had just let the original ETH pile grow without touching it.

Concrete Example: When Numbers Hurt More Than Words

Let’s walk through an actual scenario. You deposit 1 ETH at $1,000 and 1,000 USDC into a 50/50 ETH/USDC pool. Your total initial contribution is $2,000, and at that moment the pool values ETH at $1,000, matching the market. Time passes, and ETH doubles to $2,000 on centralized exchanges. Arbitrageurs start buying cheap ETH from the pool and paying in USDC until the pool’s price catches up with the outside world, all while preserving x * y = k.

By the time the dust settles, instead of 1 ETH and 1,000 USDC, your share of the pool might be something like 0.707 ETH and 1,414 USDC (numbers simplified but close to reality). The total value is around $0.707×2,000 + 1,414 ≈ $2,828. If you had just held 1 ETH + 1,000 USDC, you’d have 1×2,000 + 1,000 = $3,000. The gap — about $172 — is your impermanent loss. Notice you still made money versus the initial $2,000; you just made less than the holder.

In real life, this picture is blurred by trading fees and token incentives. If the pool charges 0.3% per trade and your share of volume is high, you might earn several hundred dollars in fees over the same period, easily offsetting that $172. The art of DeFi is deciding when the extra yield compensates for the drag from impermanent loss, and when you’re just being underpaid risk capital.

Impermanent Loss vs Volatility: Not Quite the Same Beast

Volatility is about how much the price of an asset bounces around. Impermanent loss is about how much the *relative* price between two assets has changed while your money is locked in an AMM. Highly volatile pairs usually mean higher impermanent loss, but the key is the divergence between the two assets, not raw volatility alone. An ETH/USDC pair will always be exposed to ETH’s mood swings, because USDC just sits at $1.

By contrast, a pair like ETH/wstETH (liquid staked ETH) can be very volatile in dollar terms, but the two tokens tend to track each other, so the AMM doesn’t have to reshuffle your holdings as violently. This is why people talk about best liquidity pools with low impermanent loss: they’re usually pools where the assets are strongly correlated — stablecoin/stablecoin, staking derivative/underlying, or assets that tightly track the same index.

How DeFi Users Actually Lose Money

Scenario A: The One-Sided Moonshot

The worst case for an LP is when one token moons and the other just sits there. Suppose you provide liquidity to a small-cap token against USDC. The token pumps 5x. From a holder’s perspective, this is amazing. From a liquidity provider’s perspective, the pool has been steadily selling your precious mooning token into USDC, giving you a big bag of stablecoins and a much smaller bag of the rocket coin. When you withdraw, your portfolio is more “balanced” — but in exactly the way you didn’t want.

This is why providing liquidity to your favorite speculative gem can be emotionally brutal. You think you’re supporting the ecosystem and earning yield, but you’re also systematically taking profit on the upside and buying the dip on the downside. That’s nice if you like automatic rebalancing; it’s awful if you were hoping for pure convex upside.

Scenario B: Both Tokens Bleed

What if both tokens fall together? Let’s say you LP in an ETH/MATIC pool, and the entire market dumps. Your dollar value shrinks whether you held or LP’d. Impermanent loss still exists, but it’s harder to see, because the whole portfolio is red. On paper, your impermanent loss is the underperformance versus just holding both tokens. In practice, your main problem is market risk, not AMM mechanics.

The subtlety is that people often blame “impermanent loss” for what is really just poor asset selection. If you provide liquidity for two highly speculative tokens in a bear market, AMM math is not your biggest enemy. The tokens themselves are. Impermanent loss rides on top like a fee for participating in volatility.

How to Think About Impermanent Loss in Real Decisions

Impermanent Loss as a Hidden Cost

The cleanest mental model: think of impermanent loss as a variable fee you pay for being the counterparty to traders. When volatility is low and fees are high, that “fee” is small, and the trade is worth it. When volatility explodes or correlation breaks, that hidden cost can quietly overtake your fee income. Instead of staring at complex charts, ask: “Am I being compensated enough by fees and rewards to cover this risk over time?”

This is where an impermanent loss calculator can be handy. Even a basic one that takes initial price, final price, and pool type will show you the drag from different scenarios. Plug in a 2x, 3x, 5x move and see how much you’d lose and how much fees you’d need to break even. It won’t predict the future, but it teaches your intuition very quickly.

Comparing LP to Just Holding or Lending

Whenever you consider adding liquidity, compare it against simpler options: holding the tokens, or lending them on Aave/Compound. Holding gives you full price exposure and no impermanent loss. Lending gives you modest yield with smart contract and counterparty risk, but again no AMM rebalancing. LPing sits in the middle: more yield potential, more complexity, and the special risk of underperforming your own bags.

A practical rule of thumb: if you are extremely bullish on one of the tokens and neutral on the other, LPing that pair is usually a bad idea. You’d rather just hold the bullish asset and maybe lend it out. If you are neutral on both tokens and just want yield, LPing starts to make sense, especially for correlated or stable pairs.

Practical Tactics: How People Reduce the Pain

Asset Choice: Correlation Is Your Friend

The single biggest practical lever is which pairs you choose. Stablecoin pairs like USDC/DAI or USDT/USDC historically suffer minimal impermanent loss because $1 tends to stay close to $1. You’re mostly harvesting fees from stablecoin traders, not being whipsawed by divergent prices. Similarly, ETH/stETH or BTC/wBTC pools see muted impermanent loss because the two assets are intentionally tethered.

This is why many serious LPs start with low-volatility, tight-spread pairs before experimenting with riskier pools. You’re still exposed to smart contracts and peg risks, but volatility-driven IL is much lower. If you’re wondering how to avoid impermanent loss in defi without walking away from LPs altogether, this is your foundational move: pick pairs that move together, not apart.

Concentrated Liquidity and Active Management

Modern AMMs like Uniswap v3 let you concentrate your liquidity in a price range instead of across the entire curve. That boosts fee income when price trades inside your chosen range, but also changes how impermanent loss behaves. Inside the range, it’s similar to a traditional 50/50 pool; outside the range, you end up fully in one asset and stop earning fees.

For active LPs, this is a feature, not a bug. You can adjust your ranges as markets move, turning your LP position into something close to an automated market-making strategy. In practice, this demands time, tools, and experience — and it’s easy to underperform if you’re not watching. But if you combine tight ranges with good risk management, you can improve the balance between fee income and impermanent loss dramatically.

Hedging and External Tools

Some advanced users hedge their LP exposure with derivatives. For example, if you LP in an ETH/USDC pool but don’t want too much ETH price risk, you might short ETH futures on a centralized exchange. That way, your overall portfolio is more delta-neutral: the AMM adjusts your token mix while the short position counters directional price moves. Impermanent loss remains, but you’ve separated it from general market swings.

This kind of hedging is not beginner-friendly, and mis-sizing positions can cause more harm than good. Still, it highlights an important idea: LPing can be part of a broader strategy, not just a standalone bet. When you think like a market maker instead of a yield chaser, you naturally look for ways to control risk, not just boost APY numbers on dashboards.

New Tools: Insurance and Protocol Designs

Impermanent Loss Insurance and Protocol Guardrails

Some protocols now experiment with impermanent loss insurance crypto products. The idea: if your LP position underperforms a simple hold strategy beyond a certain threshold, the insurance pays you the difference or part of it. Funding can come from protocol fees, separate insurance pools, or token emissions. This doesn’t remove impermanent loss; it redistributes it across a broader set of participants willing to underwrite the risk for a premium.

There are also AMM designs trying to bake in “IL protection” directly. For example, they might slowly vest additional tokens to long-term LPs, or adjust fee splits based on how far price has moved. These mechanisms aim to align incentives so that providing deep, stable liquidity is rewarded more than opportunistic short-term farming.

Choosing Where to LP in Practice

So where do you even begin in this maze? A pragmatic path is to start on well-audited, large-volume protocols, and to focus on pools with clear economic logic: stablecoin pairs, LST/ETH pairs, or blue-chip token pairs on major chains. “Best” here doesn’t mean zero risk, but a combination of deep liquidity, consistent fees, and assets you actually understand.

Before depositing, look at historical volume and volatility. A pool with high TVL but no trading volume is a dead pond — fees will be tiny, while impermanent loss risk remains. Conversely, a volatile pair with explosive volume might pay great fees but needs extra caution. It’s not about chasing the single best liquidity pools with low impermanent loss; it’s about finding a mix that fits your risk tolerance and time budget.

Yield Farming Without Burning Yourself

Strategies Built Around Impermanent Loss

Most yield farmers today know they can’t just fling tokens into the highest APR pool and hope for the best. Sustainable yield farming strategies to minimize impermanent loss usually involve three ingredients: correlated asset pairs, diversification across several pools, and a clear exit plan. You decide in advance at what price move or time horizon you’ll pull liquidity, instead of waiting until something “feels wrong.”

One practical trick: ladder your positions. Instead of dumping everything into one ETH/USDC pool, maybe you put some in ETH/stETH, some in a stablecoin/stablecoin pool, and a smaller slice in a higher-risk pair you’re willing to monitor. That way, even if one pool gets hit with large impermanent loss, your overall portfolio impact is cushioned by the others.

When to Walk Away

Sometimes the smartest move is to stop being an LP altogether. If you find yourself constantly stressed by price moves, manually checking on-chain charts, or second-guessing your deposits, that’s a sign the strategy doesn’t fit your temperament. DeFi offers plenty of alternatives: lending, staking, or even just holding assets you believe in.

Remember that the flashy APR numbers on dashboards rarely account properly for impermanent loss, token emission decay, or your own time and stress. A quieter, simpler strategy you can stick with is usually better than a complex one you abandon after a drawdown.

Bringing It All Together

Impermanent loss isn’t a bug in DeFi; it’s the price of turning your passive assets into active market-making capital. The AMM algorithm does not care whether you intended to trade — it will rebalance your position as prices move, and the math will compare that outcome to just holding. Sometimes you’ll come out ahead after fees and rewards. Sometimes you’ll wonder why you didn’t simply sit on your coins.

To use liquidity pools wisely, treat impermanent loss as a core variable, not a footnote. Choose correlated assets when possible, check your scenarios with basic tools, think in terms of opportunity cost versus holding or lending, and don’t be afraid to say “no” to pools that don’t compensate you enough for the risk. With that mindset, liquidity provision stops being a mysterious black box and starts looking like what it truly is: a business decision you control.